Turning Fraud Prevention into a Competitive Edge for B2B Merchants

B2B transactions that once relied on manual processes, paper invoices and long approval cycles now move through digital channels, fundamentally reshaping how businesses buy and sell. This shift has unlocked enormous growth opportunities for merchants, manufacturers and marketplaces. However, it has also created a fast-growing and often underestimated risk: B2B payments fraud.

Consumer fraud may dominate headlines, but identity fraud in B2B commerce is becoming one of the most damaging threats facing enterprises today. Fraudsters impersonate legitimate businesses, hijack accounts, open fraudulent credit lines and infiltrate supplier relationships to divert payments. While the financial losses are significant, the broader impact — broken trust, disrupted supply chains and long-term reputational damage — can be even more costly.

For B2B merchants operating in digital and omnichannel environments, fraud prevention is a core component of B2B risk management, payment security and competitive differentiation.

The Growing Reality of B2B eCommerce Fraud

Nearly 60% of U.S. businesses reported an increase in fraud year over year, driven increasingly by sophisticated schemes and gaps in legacy systems.

Global eCommerce fraud losses are projected to be $138.6 billion, and merchants lose an average of $3 for every $1 of fraud when factoring in operational costs and reputational damage.

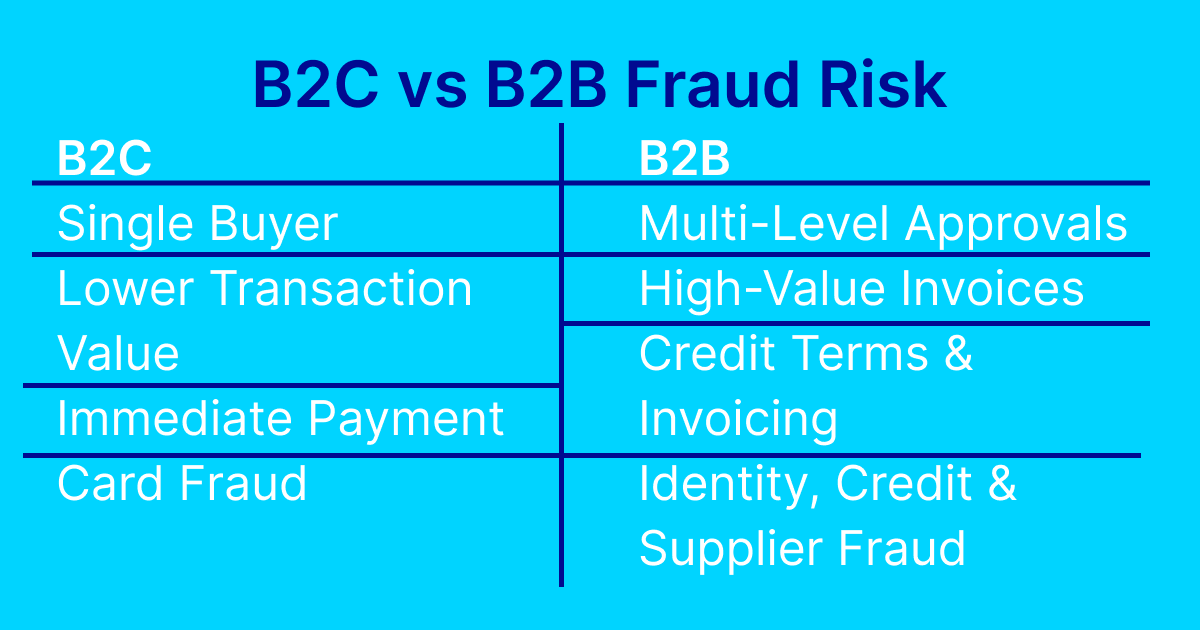

Red flags in B2B are fundamentally different from those in B2C since transactions often involve higher values and complex approval structures. As a result, a single fraudulent order or compromised account can result in losses that far exceed typical consumer fraud incidents. This makes preventing B2B payment fraud both more challenging and more critical.

Compounding the issue, many B2B merchants continue to rely on manual reviews, fragmented data and outdated controls. In a digital-first economy, these approaches struggle to keep pace with fraud tactics, creating an unsustainable combination of risk and friction.

Why Fraud Prevention Matters More Than Ever

Fraudsters exploit the complexity of B2B via onboarding processes, credit approvals, supplier verification and payment workflows to obtain goods or access credit that will never be repaid. Account takeovers and supplier impersonation are especially damaging because they can cascade through partner ecosystems.

Despite these risks, many organizations focus narrowly on reducing losses instead of building a comprehensive fraud prevention strategy that supports growth. This mindset creates blind spots which criminals are quick to exploit.

Trust is a critical form of currency today in B2B. Buyers expect secure B2B payments, fast onboarding and seamless checkout experiences. When security breaks down in any of these steps, confidence erodes and once trust is lost, it’s difficult to regain.

Reframing Fraud Prevention as a Competitive Advantage

Leading merchants are reframing fraud prevention as a competitive advantage, instead of a barrier to growth. Rather than simply stopping fraud, the objective is to build resilient, scalable systems that enable speed, confidence and long-term relationships.

Modern fraud prevention technology is critical in this shift. Advanced analytics, machine learning and real-time decisioning allow businesses to detect anomalies across thousands of data points. These capabilities support instant credit decisions and secure checkout experiences without compromising security.

These technological evolutions are especially important in digital environments, where threats change rapidly. Static rules and one-time checks aren’t sufficient; merchants need adaptive systems that continuously learn, assess risk and respond in real time.

Payments Fraud Prevention Strategies That Scale

No single tool can address every risk: leading organizations layer capabilities to create a comprehensive secure payments strategy.

Key elements include:

- Identity fraud prevention during onboarding, using business verification, document checks and behavioral analysis.

- Fraud detection tools that monitor transactions in real time and flag anomalies proactively.

- Fraud prevention analytics that provide visibility into emerging threats and patterns.

- Payment risk mitigation controls that adapt based on transaction size, buyer history and risk profile.

- Ongoing payments risk and compliance monitoring to meet regulatory and industry requirements.

By implementing composable risk models for identity verification, credit assessment and payment security, merchants can strengthen defenses while maintaining operational agility. This approach enables enterprises to focus on growth while leveraging best-in-class fraud prevention solutions.

Balancing Fraud Prevention and Growth

In B2B commerce, friction kills deals, which is why one of the biggest challenges in B2B payment security is balancing protection with experience. Lengthy onboarding, manual reviews and inconsistent approvals create frustration for buyers and slow revenue realization.

This balance can be accomplished with controls such as multifactor authentication, address verification and identity validation operating behind the scenes, reinforcing trust without increasing friction. Perfecting the balance between protection and experience is essential for B2B checkout security, where speed and confidence directly impact conversion.

When merchants master this balance, they unlock tangible advantages including the ability to offer instant or near-instant credit approvals, flexible payment options and streamlined purchasing experiences without compromising on fraud controls. That combination improves customer satisfaction, strengthens relationships and differentiates brands in competitive markets.

Fraud Prevention Best Practices for B2B Merchants

Regardless of industry, several fraud prevention best practices consistently separate leaders from laggards:

- Treat fraud prevention as an enterprise priority, not a siloed function

- Invest in fraud detection for B2B merchants that operates in real time

- Use data and analytics to inform continuous improvement, not one-time decisions

- Build layered defenses that address identity, payments and compliance risks together

- Design security to support, not hinder, growth and customer experience

These practices form the foundation of effective enterprise fraud prevention strategies. They also help organizations reduce fraud losses while enabling confident expansion into new markets and channels.

Building Trust in B2B Payments

Trust is the foundation of every successful B2B relationship: it enables buyers to share sensitive information and rely on suppliers to deliver consistently. When payments security is strong, trust grows, but when it fails, relationships fracture.

By investing in fraud risk management and secure payment infrastructure, merchants send a clear signal to customers and partners: reliability matters. This commitment becomes a differentiator, particularly in industries where long-term relationships and repeat business drive value.

Strong fraud prevention is a long-term investment: it supports building trust in payments, enhances reputation and creates confidence across ecosystems.

The Cost of Inaction

Financial losses are only the beginning of the steep costs of failing to address fraud. A single incident can trigger operational disruption, customer churn and regulatory scrutiny. Even more importantly, a damaged reputation can linger for years.

Organizations that lead fraud prevention position themselves to grow with confidence. They are better equipped to navigate uncertainty, adopt new payment models and support digital expansion without taking on unnecessary risk.

Looking Ahead

The future of fraud defense belongs to B2B merchants who view fraud prevention technology as a catalyst for growth. By combining advanced analytics, expert partnerships and deliberate focus on trust, businesses can transform a vulnerability into a competitive edge.

In a market where speed, security and confidence define success, fraud prevention for B2B merchants is a necessity.

About TreviPay

TreviPay, The Pay by Invoice Company™, is a fully managed B2B payments platform for global brands. Proven to increase AOV and reduce DSO, our accounts receivable automation software, enhanced by AI, optimizes order-to-cash and integrates with all channels and ERPs. Delivering a superior payment experience, TreviPay is the choice of top retailers, manufacturers and travel companies, including Walmart, Lenovo and United Airlines. With more than four decades of experience powering over $8 Billion in global trade, TreviPay was named a Leader for Embedded Payment Applications by IDC and a top vendor in cash application by The Hackett Group. To experience Zero Touch A/R, visit www.trevipay.com.